Timing is everything when converting clients from term to permanent insurance.

By Michael BertonYou’ve just finished gathering and analyzing the financial and lifestyle information for a new client, Sarah, and made the initial determination she should acquire a life insurance policy worth $500,000. But what type?

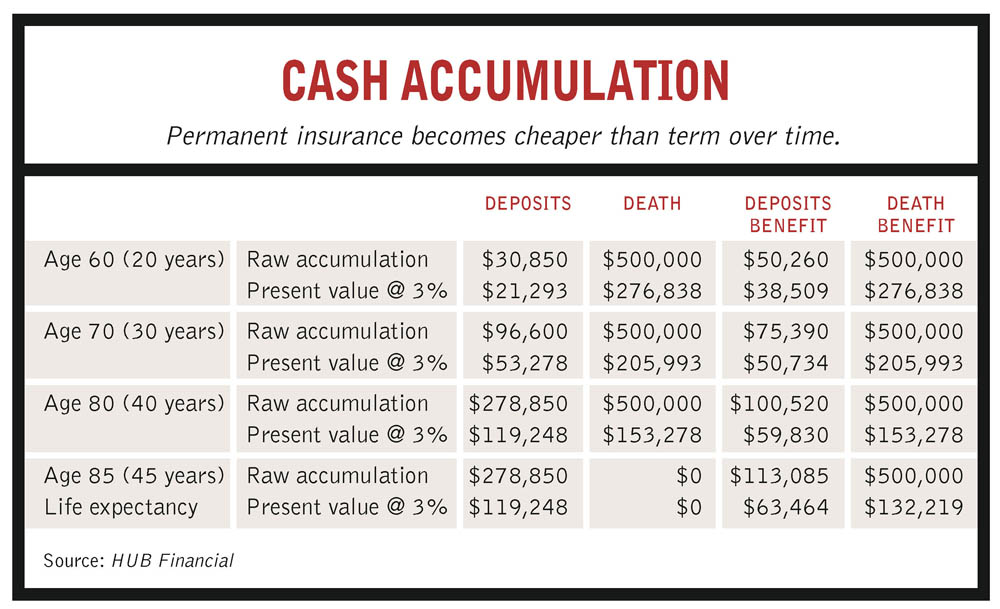

You get some quotes from the life insurance companies for a 40-year-old female non-smoker and they present you with two options: a $500,000 Term 10; or a Term 100 permanent policy of equal value (see chart).

Obviously, if Sarah’s need is temporary, (20 years or fewer) she’ll pay less for the term policy.

But if her needs are longer- term, the permanent solution becomes less expensive over time and will last as long as she continues to pay the level premium. If Sarah can’t currently afford the $2,513 permanent premium, she could choose a term policy containing an option to con- vert to a permanent policy of equal face value at a later date. But the premium on that policy would be priced at future rates and not the $2,513 currently being quoted. To evalu- ate the two options, simply look at what she’ll pay over time (see table) and compare the total premiums paid; net present value of those premiums; and the death benefit differences between Term 10 and Term 100 policies.

Even though permanent insurance makes good sense in a lot of situations, many advisors still aren’t selling it. Why not? Simple. Clients inherently dislike talking about death and are reluctant to have the discussions necessary to make proper planning decisions. Further, many of today’s advisors were not trained in the traditional life insurance industry, and are not strongly tied to a life insurance company that offers formal training.

While these advisors readily see the importance of assisting clients with risk management issues, they often find the dazzling array of permanent products complex. Even if they devote the time to understand the products, the job of clearly articulating the concepts to clients can be daunting. In addition, the insurance industry continues to assail advisors with an array of new, non-traditional products that compete for a share of the client’s wallet, such as long-term care (LTC) and critical illness (CI) coverage. Being out of touch for even a year or two can leave an advisor far behind his competitors in product knowledge, new features, investment options, taxation issues and the like.

If the advisor sold a permanent product, he or she must monitor the client account continually to ensure the policy performs as anticipated. For example, a universal life (UL) policy may originally have been issued with yearly renewable term (YRT) to allow greater cash dump-ins with an eye toward a later switch to level cost of insurance (COI). Advisors will have to monitor the policy to ensure the planned cash dump- ins are actually made, and to properly time the switch to level COI to contain the rising premium costs. If this isn’t done right, the policy may be under- funded and unable to support level COI without significantly increased premiums, a huge cash dump-in, or a reduction of the death benefit. If the problem remains undetected, the policy could lapse and expose the client to a reinstatement application, higher premiums, or if his or her health has deteriorated, a possible declined application.

It’s also hard to balance the advisor’s need to book securities purchases with term (YRT) to allow greater cash dump-ins with an eye toward a later switch to level cost of insurance (COI). Advisors will have to monitor the policy to ensure the planned cash dump- ins are actually made, and to properly time the switch to level COI to contain the rising premium costs. If this isn’t done right, the policy may be under- funded and unable to support level COI without significantly increased premiums, a huge cash dump-in, or a reduction of the death benefit. If the problem remains undetected, the policy could lapse and expose the client to a reinstatement application, higher premiums, or if his or her health has deteriorated, a possible declined application.

It’s also hard to balance the advisor’s need to book securities purchases with the client’s need for appropriate insurance coverage. The old adage “buy term and invest the rest” conveniently suits those who must meet sales expectations on the investment side. The problem is allocations often tilt toward securities, so clients end up raiding the investment portion to meet increased expenses or pay for emergencies—when it would have been easier to borrow against insurance policies with built-up cash value. Further, the investment portion will be subject to ongoing capital gains taxation, eventually to probate tax, and possibly to wills variation if the heirs get into a dispute. Advisors need to show clients there is value in the forced savings, tax shelter and estate bypass that a permanent insurance plan provides.

Of course, for many clients, term is the ideal product. It certainly is easier to understand and our primary job is to ensure the right death benefits are available. Younger clients, who are cash-strapped while raising families and paying mortgages, have a critical need for the right amount of life insurance at the lowest possible premium. As with Sarah, we can provide a bridge to future needs by including a conversion option allowing for a later switch to a permanent policy without having to take a medical exam. The strange thing is that such plans are rarely converted, according to Judy Simpson, regional vice-president of insurance brokerage HUB Financial in Vancouver. “They are frequently terminated or replaced by more modern, often cheaper term policies, rather than being converted to permanent plans,” she says.

The best place to start is by fully assessing the client’s current and future needs, and how they’ll relate to risk tolerance over time. The exercise will produce a modular financial plan that includes the client’s goals, assets, liabilities, family income sources and lifestyle expenses. Determine if the client’s risks are short- or long-term, or combined.

Temporary needs might include coverage for a mortgage, car loan or key person in a business. Permanent needs would include providing for capital gains tax, disabled dependents, final disbursements (including taxes), bequests, funding a business succession or passing down the family cottage.

More affluent clients, like business owners or wealthy retirees, have different insurance needs. They have to think about coverage for debts, taxes and often income replacement. Will the client have the same requirements at age 65 as they did at age 40? Likely not, so a base level of permanent insurance with a temporary term insurance rider may best do the job.

You may have studied the basics of the permanent policies and be inexperienced with the product details and how to present them. Or perhaps your skills are just rusty. If that’s the case, you’ll need to hit the books and gain a better understanding of the products you sell and what your illustration soft- ware can and cannot do for you.

All three main permanent plans have their place: Term to 100; whole life; and UL. In the case of the latter two, do not allow the added dimension of the cash value to cloud your analysis. You must investigate the costs and risks associated with the potential growth of the cash value in those plans, as well as the actual cost of insurance and the administration and other fees within the plans.

A plan with cash value will allow you to support the cost of insurance over time, but that cash only becomes avail- able to the client if you terminate the permanent insurance. Keep in mind that what you’re actually building is a risk- management program, so use a conservative rate of return in the range of 3% to 4%. This is especially important if you plan to “quick pay” the policy. Using lower expected returns also avoids the notorious conditional performance bonuses lurking in many illustration programs—these can produce an overly optimistic outlook and lead to disappointments for clients and liability risk for the advisor.

Many advisors who are uncomfortable with the higher insurance costs and riskier investment options of a UL contract choose whole life, especially for 15- or 20-year pay plans. Removing investment options in favour of insurance company policy dividend performance will take away investment anxiety for many clients and advisors. It also makes the product presentation easier.

There is still some risk, but it’s much less than a stock index. T-100 removes all investment risk, but also leaves no cash value if the plan is terminated. Ultimately, the anticipated time span, premium level and death benefit will determine which plan is most efficient.

Learn or review the various marketing concepts available, such as the estate bond, insured retirement plan or pension maximization strategies. To gain ease with these plans, consider working with an experienced insurance advisor or a marketing specialist with your MGA or manufacturers.

Many won’t even make you share the commissions. If you don’t have a management system for your insurance business to equal the one you have for securities, get one. There are a number of client management software products, such as CPU Tracker, that will bring discipline to your practice. Dig through your file drawers and review your clients’ coverage. Some MGAs will even refer a marketing specialist to help you get started.

If the process doesn’t fit the approach of your practice, then refer clients to an insurance specialist who may share commissions and the analytical load. Make sure the risk management strategy is implemented and that you haven’t left an opening for a competing advisor. Whether you use someone else or do it yourself, double-check that proper insurance recommendations are made. You can’t just blow this off, since the liability for non-action can be considerable. Finally, remember your clients’ heirs are relying on you as well.

This article appeared in The Advisor’s Edge magazine, May 2006

{kind=link}

{kind=link}

{kind=link}