Retirement compensation arrangements can help employers lure and retain executives and other key employees.

by Mike Berton

Times are tough for employers and business owners who want to build retirement packages to attract and retain top-notch professionals.

Employee stock option programs, which created fortunes in the 1990s, have lost their lustre, and challenging business conditions threaten the security of future compensation.

Even the certainty of the long-cherished defined benefit pension plan seems at risk. And this has led to a re-emergence of interest in the retirement compensation arrangement (RCA).

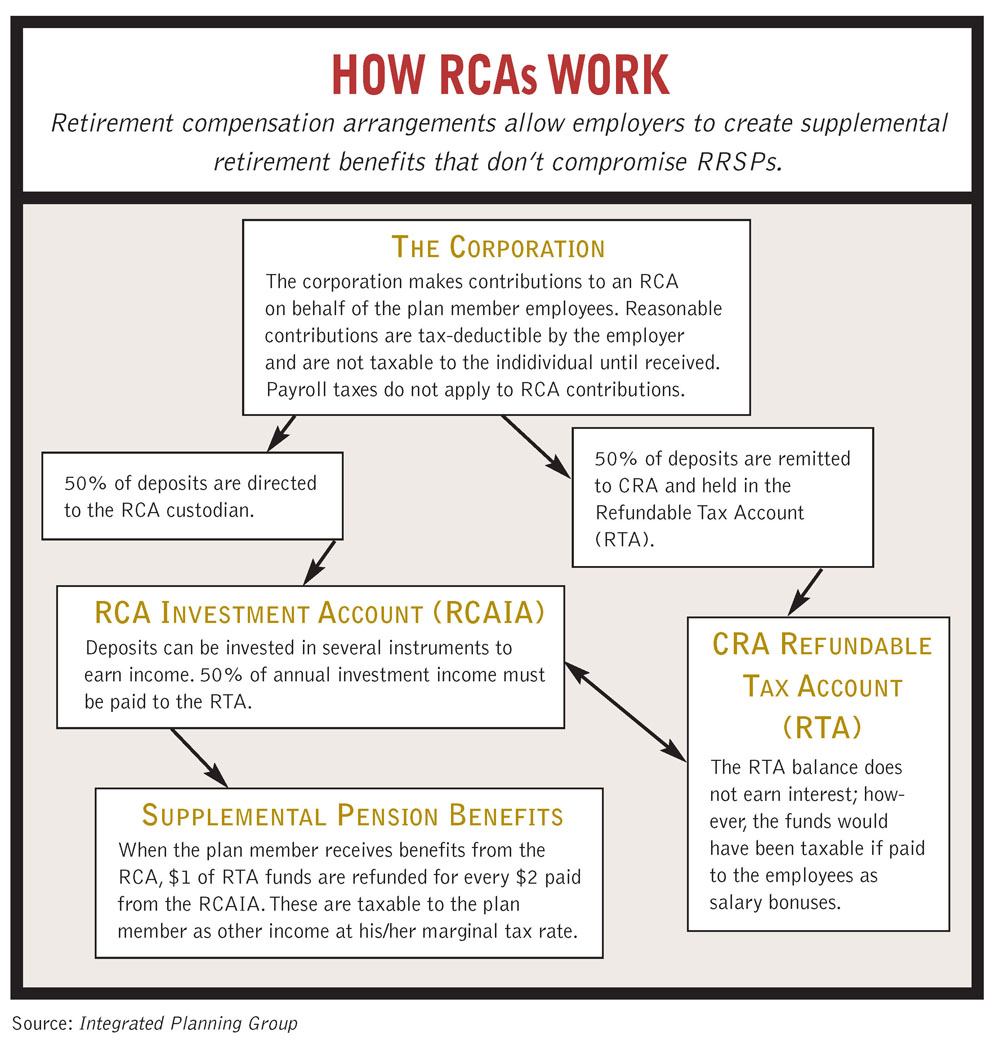

Introduced in 1986 when personal rates were around 50%, RCAs were intended to place non-registered pension plans on the same footing as paying bonuses. Governed by rules contained in subsection 248(1) of the Income Tax Act, RCAs are non-registered retirement savings plans that provide members with supplemental retirement benefits without compromising the integrity of their RRSPs or other registered plans. Employer contributions to an RCA are tax-deductible to the employer, but they are not a taxable benefit to the member employee. But there’s a hitch.

To neutralize any tax advantage these arrangements might have over the old-fashioned bonus-out strategy, the tax rules require payment of a special refundable tax. The amount of that refundable tax equals:

- the aggregate of 50% of all contributions for the year and previous years;

- plus 50% of the net income and net capital gains for the year and previous years;

- less 50% of all distributions and benefits paid out to the plan member.

These funds must be paid to a non-interest-bearing Refundable Tax Account (RTA) held by the CRA.

The remaining 50% of the employer contribution is held in an RCA Investment Account (RCAIA) administered by a custodian (often the employer). The account can essentially hold any type of investment and, under certain rules, a cash-value life insurance policy or life annuity.

This is a retirement pension, so funds in an RCA trust can be paid to the employee upon retirement, termination or death. For every 2 dollars paid out of the RCAIA, the CRA will refund $1 from the RTA. Payments received by the plan member are included in income as “other income” in the years they are received (s. 56(1)(x)). There is some relief: Payments out of the plan that qualify as retirement allowances may be transferred to either an RRSP or RPP subject to contribution limits under paragraph 60(j.1). Benefits paid out of the plan at the member’s death are taxable either on the plan member’s final return or as a “right or thing” (s. 70(2)). There are many benefits of an RCA to high income-earning owner-managers, shareholder employees and executives:

- It creates a pension in excess of the statutory pension limits.

- There’s potential immunity for the beneficiary from business insolvency, new management arrangements or changing personal conditions.

- There may be tax efficiency if the employee enjoys a lower tax bracket in retirement or intends to retire in a lower tax jurisdiction.

The employer can benefit by establishing an RCA as well. It can:

- attract and retain key employees by offering a special pension supplement;

- gain flexibility in the timing and amounts of contributions and payouts;

- provide the employee with a written agreement concerning the amount, timing and frequency of the contributions;

- customize the design of the plan to suit unique circumstances;

- choose who will benefit;

- potentially reduce payroll taxes;

- reduce corporate profits with the tax-deductible RCA expense (effectively funding post-retirement benefits with tax-deductible dollars today);

- enjoy the tax deduction and achieve lower corporate earning levels that put the company in a better position to access the small business exemption for a future sale;

- have confidence the contributions made on behalf of the employees to the RCA are safe in the hands of the trustees; and

- potentially borrow against the RCA and use the funds to finance operations.

An RCA also can provide some benefits for business owners who are planning for succession. Large contributions to an RCA prior to an anticipated sale will reduce the value of the business, making it more affordable for a child or other family member. Such a provision also reduces, at least in part, a need for the new owners to provide continuous income to the retired owner. And the retired owner is secure in the knowledge the bulk of his or her nest egg is safe from the future business fluctuations.

Complex rules, outlined in subsection 207.6 (2) of the Act, govern the use of an exempt life insurance policy in the RCAIA. An exempt life insurance policy does not normally produce taxable earnings that would give rise to annual refundable tax. That allows the insurance cash value to compound without taxation. And should the plan member die, the death benefit will be paid to the trust without creating

refundable tax, and the payment in turn will produce a refund to provide survivor benefits. To make it so the beneficiary does not have to pay income tax on the benefit received from the trust, a split-dollar insurance arrangement would have the death benefit owned by the company as a key-person plan or by the individual personally. At the same time, the RCAIA would hold the accumulating cash value. This removes the cost of life insurance from the RCA and creates a tax-sheltered investment account in the RCAIA.

As the employer is required to pay refundable tax to the CRA, it must contribute twice the amount necessary to pay the premium. While the promise of greater tax efficiency is a worthy consideration, bear in mind the insurance policy has a cost, too.

Controversy surrounds the use of front-end leveraged RCAs. Let’s say XYZ Corporation has $3 million of active income left inside the corporation after salaries and expenses. The owner-shareholders would like to purchase another building, and plan to bonus out the money and then lend it back to the company.

This will help the company access the lower corporate rate. The only problem is they will only net 53.6% of the money after paying personal and corporate income tax. But by using the leveraged front-end RCA, they can avoid this problem. The $3 million is contributed to an RCA on the owner’s behalf and deducted from the company’s income for the year. That eliminates corporate tax. The RCA trustees procure a loan of 90% of the total contribution (based on the value of the trust assets and the refundable tax account) from a financial institution.

The RCA then lends this money ($2.7 million) back to XYZ Corporation. CRA is on record questioning the existence of an RCA in circumstances where funds intended for retirement are lent back to employers. A negative ruling by CRA with attendant denial of deductions to the employer as well as penalties and interest could be costly. Those considering this structure should get both an accountant’s opinion and an advance ruling from the CRA.

Not just anyone or any company is a reasonable prospect for an RCA. The key market seems to be senior executives. The 50% tax rate, although refundable, makes the RCA less tax-efficient for people who own their own companies. For many of these people, it may be better to simply pay themselves a bonus and invest the funds.

Advisors should pre-qualify potential clients as:

- shareholders and owners of corporations, or key executives;

- incorporated professionals with T4 earnings in excess of $150,000;

- employers who want to attract key employees and retain them with golden handcuffs;

- employees who might wish to manage or reduce certain kinds of bonuses;

- those with considerable past service with the company;

- executives and business owners with individual pension plans;

- businesses with profits in excess of the $300,000 small business limit;

- businesses expanding through internal growth or acquisition; or

- executives, professionals and business owners who will likely retire in a low-tax jurisdiction outside Canada.

The company’s board must pass a resolution to establish the plan and a trust agreement drafted (without the agreement, it will be deemed a trust under subsection 207.6(1) of the Act with the employer deemed trustee). The employees must confirm the plan benefits and the RCA must be registered with the CRA (form T733) along with a valuation report as of the effective date.

Set-up fees for a simple RCA range in the $5,000 area, but climb steadily per participant. In addition, an RCA requires ongoing maintenance, including:

- annual reporting, along with an RCA contribution summary (T737-RCA) and RCA tax return;

- annual member statement;

- review of investments;

- periodic valuation;

- document maintenance;

- record keeping; and

- filing T3-RCA within 90 days of the calendar tax year.

A review of several trustees reveals a wide range of annual trustee fees. For a simple RCA, an annual average seems to fall at about $2,500, plus an investment management fee which might range in the area of 2%, depending on the investments chosen.

The RCA rules are complex with serious implications if errors or omissions are made. Care must be taken to avoid the application of the Salary Deferral Arrangement (SDA) rules, which put off payment of salary to a future date. If an RCA is set up and funded with amounts that loosely match a reduction in salary, the SDA rules will apply, denying the tax-deductibility of the plan retroactively.

Advisors should seek professional pension consultants to assist them in the establishment of these plans. Such a firm or individual would be an excellent addition to your team of external consultants.

Michael Berton, CFP, CLU, R.F.P., FMA, is a financial planner with Assante Financial Management Ltd. and part-time instructor at the B.C. Institute of Technology (BCIT) in Vancouver. The opinions expressed are those of the author and not necessarily those of Assante Financial Management Ltd. or BCIT. This article originally appeared in Advisor’s Edge magazine, February 2005. Reproduced with permission.

{kind=link}

{kind=link}

{kind=link}

{kind=link}